Lather, rinse, repeat?

The major market news of the month was the re-election of Donald Trump as the 47th President of the United States of America. Not only did Trump secure a clear victory, but the Republican Party also achieved a ‘clean sweep,’ gaining majorities in both the House of Representatives and the Senate.

His success wasn’t exactly a surprise. The pre-election betting markets pointed to a decisive Trump victory, and while the polls were much closer, they did correctly favour Trump and the Republican Party.

But is this a game-changer? Trump is the master of the campaign trail, but whether campaign rhetoric promising a sea change in both domestic and foreign affairs translates into official policy is still unknown.

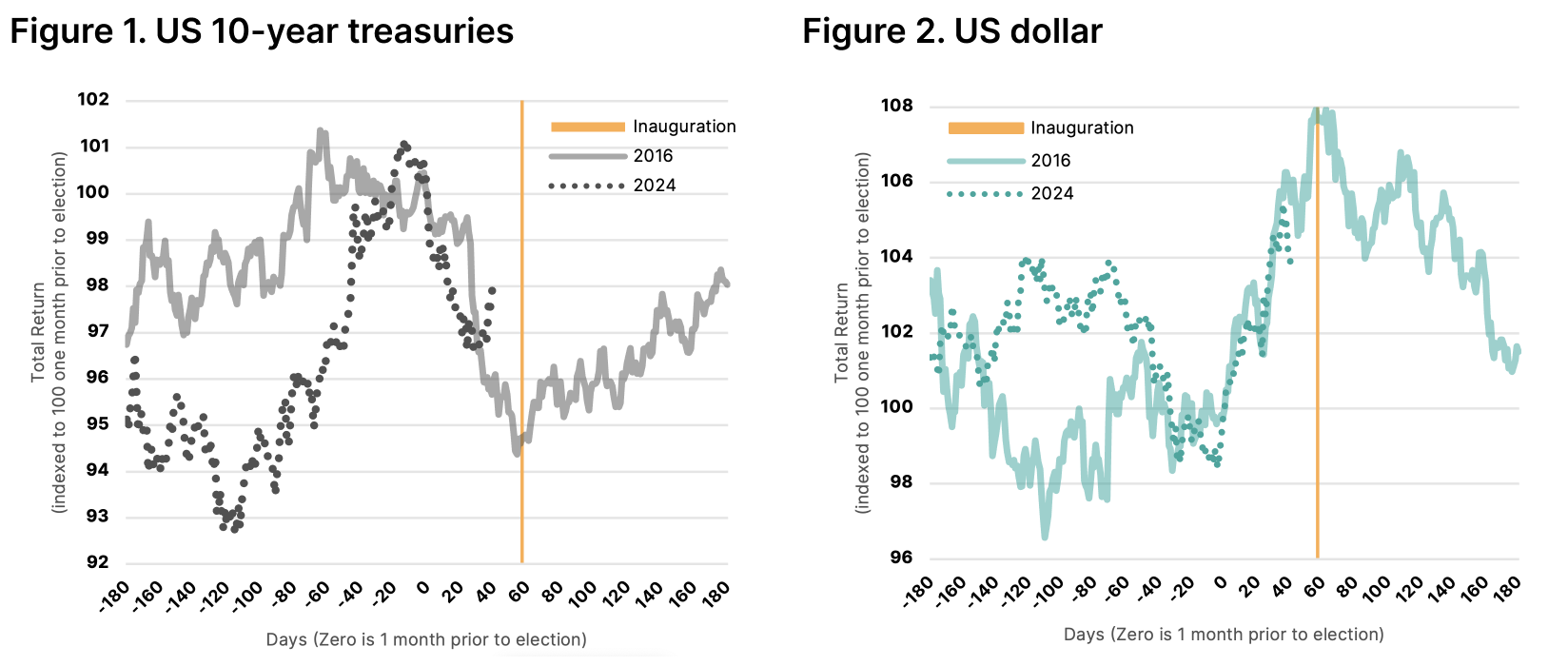

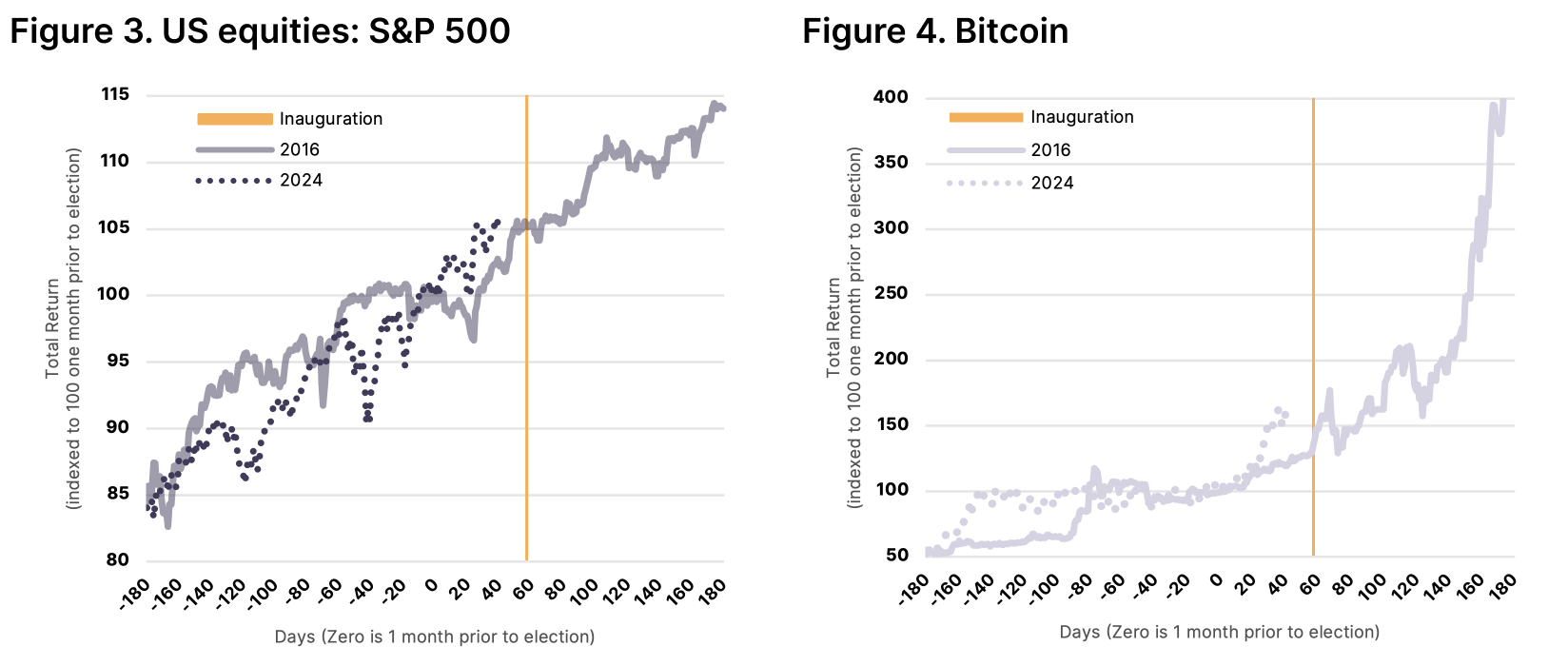

In general, Trump’s previous presidency was a positive driver for markets, as he slashed regulations and reduced corporate tax rates, boosting profits and ultimately share prices. To gauge how optimistic investors are about Trump’s presidency this time around, we track several assets that should benefit from or suffer due to his MAGA policies, comparing them to their performance in 2016. The charts below paint an interesting picture of the major asset classes:

US treasuries: 2016 path suggests further weakness into the inauguration date;

US dollar: 2016 path suggests further upside potential into the inauguration date, then reversal;

US equities: tracking in line with 2016, with potential for further gains in the months following inauguration;

Bitcoin: tracking ~40% higher than 2016 rally, so potential for some short-term reversal before rally.

Source: Human Financial, Bloomberg. Data since 1989, apart from Bitcoin since July 2010

A single historical occurrence is not sufficient to establish an investment law, just as we should not take any politician's campaign promises as definitive policy. However, the charts above do suggest that, based on 2016, there is potential for further rallies in US shares and crypto, while the US dollar rally may be short-lived and US treasuries could face additional challenges.

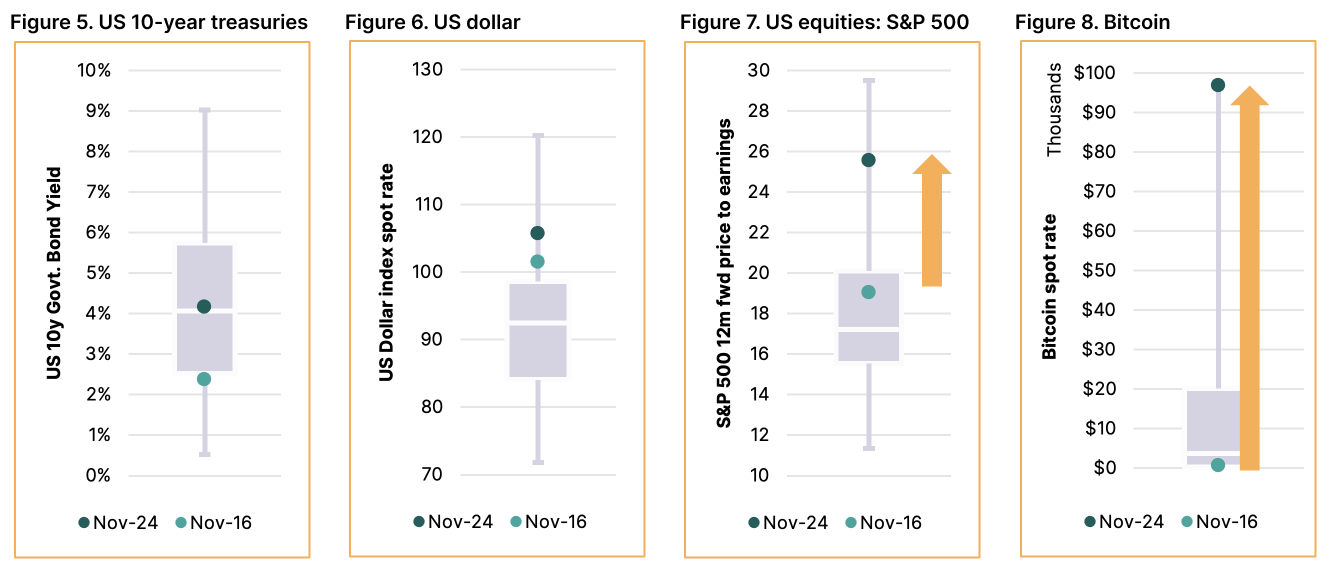

That said, when examining the current valuations/levels of these assets, a different picture emerges. Valuations across assets can be complex. For treasuries, we’re using yield; for the US dollar and Bitcoin, we’re using spot rates; and for US equities, we use the 12-month forward price-to-earnings ratio.

US treasuries: 10-year bonds are yielding nearly 2% higher than when Trump was elected in 2016. This represents the average yield over the past three decades, suggesting that Trump’s increased spending plans are not fully priced in by investors.

US dollar: The US dollar is trading 4% higher than in 2016 which puts it in the 90th percentile over the past three decades. This suggests a lot is in the price and outside of a major negative shock, further USD gains may be limited.

US equities: When Trump was elected in 2016, investors were paying 19 years’ worth of earnings in price. Today, investors are paying over 25 years’ worth of earnings for S&P 500 stocks, equating to the 96th percentile over the past three decades. The only times US stocks have been more expensive were prior to the bursting of the dotcom bubble and in the immediate aftermath of Covid when earnings expectations were still supressed.

Bitcoin: The numbers on this asset are eye-watering. When Trump was elected in 2016, Bitcoin finished the month trading at $743. Today it sits at a record high of $97k. Bitcoin has rallied >50% over the past two months, and it has more than doubled this year. Can Bitcoin reasonably be expected to benefit from the same Trump tailwind when it is trading 130x higher than it was in 2016?

The combined analysis suggests that investor expectations are already elevated and are sky-high in some instances. Trump’s pro-business campaign promises may already have been more than fully factored into asset prices. We should take note of legendary investor Warren Buffet’s maxim that “Price is what you pay, value is what you get.”

The above analysis has focused on the impact of the US elections and does not provide the complete picture of our view. However, it should be mentioned that there has also been notable underperformance in markets that could be negatively impacted by trade tariffs. While we won't know the full impact until Trump takes office in January, the degree of underperformance is already starting to create attractive entry points.

Due to the potential for additional volatility around year end we are preferring to express our tactical views via currency, due to the speed with which we can execute. In November, we took advantage of post-election market movements by hedging USD currency exposures in our actively-managed global growth portfolios, selling as the US dollar rallied, and thus capitalising on more attractive levels. We remain patient but opportunistic, scanning for opportunities in unloved assets.