The bear in bull’s clothing

Equity market returns for the second quarter were decidedly mixed across the board. While the US tech mega cap-heavy Nasdaq delivered an 8% gain, at the other extreme French equities plummeted 7.1% as hard right-wing gains became evident in the country’s snap elections. Meanwhile, here in Australia domestic equities were weaker, with the local ASX 200 index falling -1.1% over the quarter. Interestingly, the ASX resources sector (-8.7%) has underperformed banks (+17.3%) by a whopping 26% YTD, dragged lower by investor concerns about the impact of China’s weak property sector on iron ore prices.

This high level of dispersion across developed countries and across sectors could be signaling a change of phase within the economic cycle, in which investors are switching from optimism and greed to reevaluation and caution. For example, a score check ‘under the hood’ of the stocks that make up the ASX 200, shows that 59% of companies within the index are not beating the YTD index return of 4.2%. In fact, 49% of stocks within the index have a negative return so far in 2024 and only one stock in the ASX200 was sitting at a one-year high: neither of these stats are underlying signs of upwards momentum…

The numbers are similar for the US S&P 500 where 75% of stocks within the index are lagging the index return of 15.3%; while 37% of companies are delivering negative YTD returns as at end of June.

Concentration risk

Stock markets are not uniform beasts. As we’ve seen, there are significant sector disparities in performance. Beyond that, we also see the emergence of concentrated thematic opportunities. In the last year the most pronounced theme has of course been the rise of artificial intelligence (AI).

But AI, too, is not a guaranteed ticket to widespread gains. The huge winner of the recent AI boom is well known: poster child NVIDIA has seen its share price rise by over 2,800% over the past five years, from around USD 4 per share to a peak in June of over USD 135.

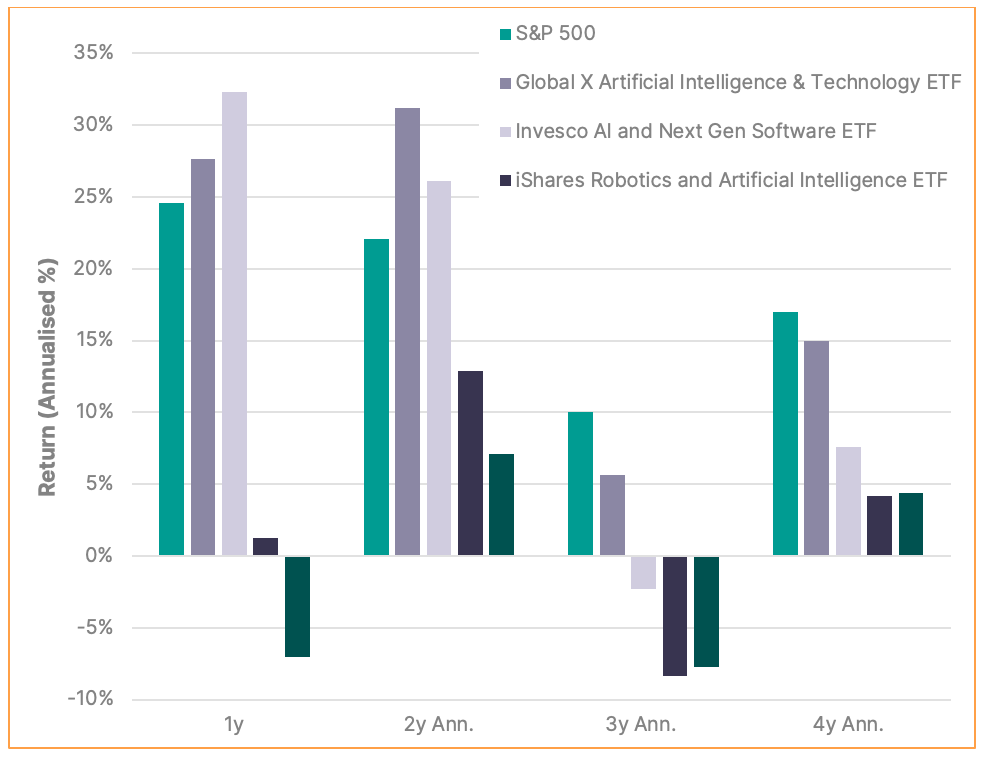

But has this breathtaking performance been replicated elsewhere? To check in on the breadth of AI gains, we analysed a number of the larger US-based AI-focused ETFs.

Despite a large degree of crossover in the stocks they hold, their performance has been mixed. The two ETFs that include robotics have delivered poor results over the last four years. The other two have both outperformed the S&P 500 over the past two years; however, they both lag over three and four years.

This highlights one of the underappreciated facts of high growth companies – while they can grow exponentially, their share prices can be quite volatile. For example, while NVIDIA has delivered huge gains over the past five years, it has also suffered four >-20% selloffs, including one in 2022 in which it lost nearly 2/3rds of its value.

Figure 1. Select artificial intelligence ETF performance vs S&P 500

Source: Human Financial, Bloomberg

Turning to individual stocks within these AI thematic ETFs, in an AI bull market we would expect the returns to be both (a) large, and (b) widespread within an index that is designed to capture the returns from companies targeting AI business activities.

We’ve taken the Global X Artificial Intelligence & Technology thematic ETF as an example, and analysed its underlying holdings. To give the individual stock performances some perspective we have compared them to the S&P 500, using the SPDR S&P 500 ETF (SPY US) as a proxy.

It’s instructive to do this both as at 31st December 2020 after the previous post-Covid large market rally; as well as for the current market situation.

In 2020, AI was also a hot thematic, generating a widespread list of winners within the Global X Artificial Intelligence & Technology ETF nearly tripling the S&P 500 with a 54% return for the year. Nearly 60% of the companies beat the S&P 500 return, which in itself was a healthy 18.35%. There’s no precise rule for such things, but these impressive numbers are what most would expect during a period of strong returns within a thematic.

Figure 2. 2020 calendar year performance of companies in the Global X Artificial Intelligence & Technology thematic ETF

Source: Human Financial, Bloomberg

Fast forward to end-June 2024 and we’ve had another AI wave, but this time dominated by NVIDIA’s stellar rise. Running the same analysis on Global X Artificial Intelligence & Technology ETF paints a very different picture from 2020. The ETF has returned 14.75% YTD, which lags behind the S&P 500’s 15.3%. Of the companies within the ETF, two-thirds have failed to beat the return of the S&P 500 and a whopping 45% have actually suffered share price declines.

Does this suggest that AI is overblown? This analysis suggests that the AI wave may actually be more about an NVIDIA wave, and that investor exuberance gives way to a lower, more rational repricing of the market.

Figure 3. 2024 YTD performance of companies in the Global X Artificial Intelligence & Technology thematic ETF

Source: Human Financial, Bloomberg

Slowing down

From where we sit, the global economy appears to be entering a slowdown phase. The easy gains are behind us and it will become increasingly difficult to generate growth as long as interest rates remain at current levels. The inflationary impulse across the world is divergent with prices reaccelerating in Australia and the US, even as they are falling in Europe, Canada and emerging markets.

In the EU and in Canada, lower growth and higher unemployment have combined to prompt their central banks to make single interest rate cuts. We continue to see this as a response to the weaker economic outlook rather than a positive due to normalising inflation levels.

Despite this outlook, it appears that investor risk appetite remains unperturbed, despite clear evidence that current market levels are dominated by the outperformance of a few mega stocks. The performance of the wider market suggests that a sea change is already upon us.

Our view is that while FOMO is ever-present, we should remain cautious. The future is likely to be more challenging than current markets suggest.